Can I Self-Insure My Future Lengthy-Time period Care Wants with My Present Monetary Property? – Half 1 of My Singapore LTC Notes

After my dad handed away virtually two years in the past, I took a while to mirror upon the place I used to be financially. This reflection is to assume onerous about what I want, the diploma of flexibility I want, how a lot is sufficient and what are the configuration.

I feel I ought to have greater than sufficient belongings and I feel a few of you may additionally be in that place. Is it essential to essentially know when you have sufficient? Effectively, I’m not positive about you, however it doesn’t bug me that a lot however I feel it prevents me from diverting extra sources to different causes like charity or giving.

I lined

- my important spending and the way a lot to fund it,

- the life like primary ongoing spending to offer a sure respectable life-style and methods to fund it,

- preparing a sinking fund for all my future insurance coverage premiums (earlier than this text),

- a sinking fund for my future medical health insurance premiums,

- a sinking fund to fund potential main finish stage essential disaster,

- estimating how a lot doubtlessly to put aside for my nephew’s future training (from now until college) if I want to.

There’s an unsettling space that I’ve not lined, which is what occurs if I’ve some long run incapacity subject later in life, with the prospect that I might have to remain in a nursing house.

I feel singles might have to consider this extra as a result of we don’t have plenty of caregivers, and we additionally don’t need to be such a burden to them, after they produce other household wants and duty. I feel I don’t need to give it some thought partly as a result of fascinated by it form of makes it extra prone to occur to me.

Secondly, out of all of the objectives, I felt that that is the toughest monetary aim to get funded, apart from fulfilling your different monetary objectives. Lastly, I’d often get some thread of inspiration to discover sure subjects and that has not occurred but.

This yr one challenge that our options crew must take care of is to evaluation how we information our advisers to plan or have a dialog about their long run care wants. So I used to be compelled to confront this troublesome subject. The by-product of this job is typically it’s relevant to my private life.

I’m fairly pleased I accomplished this challenge this yr personally as a result of doing the work assist make clear my present scenario. It may not imply I’m doing okay. Typically figuring out you will have an issue is definitely a great factor.

On this publish, I’m going to speak round long run care wants from my very own perspective. The route I finally take applies to my very own scenario and isn’t a steering how we plan for our shoppers as a result of I could also be prepared to just accept some trade-offs whereas usually they won’t.

That is probably Half 1 out of some elements. The primary half is about whether or not we will self-insure our manner out if we now have satisfactory belongings for not simply our monetary independence, different essential objectives but additionally for our long-term care wants.

Okay, this text goes to be lengthy.

For these of you who don’t need to learn in regards to the analysis behind why we have to take into account long-term care and need to zoom into my private answer, begin studying from the “Private Reflections about Lengthy Time period Care After Wanting on the Analysis”.

What are Extra Difficult Disabilities?

Every now and then, we would undergo from discomfort that stop us from doing one thing. After I damage my again or piriformis lately, I couldn’t put on my pants or socks correctly, can not bend down.

These are short-term incapacity however jogs my memory the results if it will get worst. Being single and alone, I understand that I’ve to be further cautious with my harm and actually have to seek out bizarre methods to put on the socks with out hurting.

The official definition of incapacity is if you happen to can not do any of those six issues: bathing, dressing, toileting, transferring (getting out and in of mattress),consuming and continence. These are Actions of Each day Residing or ADL for brief.

You’ll be able to argue that I’ve develop an ADL associated to dressing however to not the prolong I want one other individual to assist me.

Often in case you are injured, you may seek the advice of with an occupational therapist to evaluate what number of ADLs you checked off. You can get a physician however the physician might not be as specialised to evaluate as an occupational therapist.

There’ll come a time after I need assistance. Throughout each my mother and father final phases, they can not get away from bed, can not shit, can not tub, can not costume.

In line with most definition that’s eligible for insurance coverage claims, it is advisable fulfill 3 out of the 6 ADLs. There are personal plans that permit you to declare if you happen to meet 1-2 ADLs.

I convey this as much as allow you to see the diploma of severity. In line with my occupational therapist buddy, the distinction between two and three ADLs is much less clear and so the distinction in hole just isn’t as large.

But there are folks with solely two ADLs, which can imply they may or may not be capable of declare the incapacity insurance coverage.

Understanding Extra About Disabilities in Singapore

Not all circumstances of incapacity is so dramatic that lands you in a vegetative state or have to examine you in to nursing care.

The next exhibits the rating lf completely different group of incapacity and the way the rating modifications over time.

That is carried out within the Burden of Illness research by NUS, along with College of Washington. This research seems to be at how longevity and incapacity have advanced from 1990 to 2017.

We noticed that the incapacity that ranks the best doesn’t change a lot, however I need to present this desk to not present how the rating modifications however what sort of incapacity which might be on the market.

A greater illustration will likely be this one, which exhibits the proportion of incapacity that dominates completely different age group.

I’ve labelled just a few bigger proportion ones.

Let me checklist down what makes up among the bigger classes.

Cancers:

- Male: Lung, colorectal, liver and prostate.

- Feminine: Breast and reproductive system cancers.

Neurological problems:

- Alzheimer’s illness and different dementias

Psychological problems:

- Autism spectrum problems

- Nervousness problems

- Depressive problems

- Consuming problems

Unintentional accidents:

- 50% Falling

- 50% different causes

Sense organ ailments

- Imaginative and prescient impairment corresponding to glaucoma, cataracts and macular degeneration.

This chart exhibits us that incapacity might not be an finish stage factor. You will have acquaintance or pals of acquaintances who can not work resulting from psychological issues corresponding to melancholy. On this research, this can be a incapacity however it may not fulfill any of those ADL. It isn’t long run sufficient as properly.

Those we’re extra involved with are those in later stage which is most cancers, neural, muscular skeletal.

These are the incapacity that could be long run and need assistance. It is usually potential to undergo from this earlier within the instance of an unlucky accident.

I pay attention to each and that is how I body the well being downside:

This may assist us break down which danger we’re defending towards into two phases:

- Section 1: The low possible however excessive financial and energy influence incapacity.

- Section 2: The excessive in all probability and comparatively excessive financial influence and excessive effort influence incapacity.

The reduce off between every part is subjective.

Each phases are excessive influence as a result of within the worse case, we’d like assisted assist, remedy which might value fairly a sum of cash over time. At any time when the occasion happens or recurs, we would not be capable of faucet our revenue meant for different important functions.

The distinction between the 2 is that there comes a time once we are older that that is a lot possible.

My mother suffered for 1.5-2 years of some type of incapacity earlier than passing away. My dad was principally in mattress for the final half yr. If in case you have a mum or dad affected by dementia, you’ll understand they’re useful apart from the neurological points and so they survive for some years.

The care value for each mother and father are taken care by my brother and me, the caregivers. And that may be an choice however I feel if you happen to love your potential caregivers sufficient, you may need to take into account when you have taken care of your long run care wants earlier than it occurs.

Bryan (my crew member) and myself thought of three issues:

- How possible are we disabled when younger?

- and for a way lengthy?

- If we undergo from incapacity youthful, does that shorten our life expectancy?

We didn’t get good solutions on this space after our analysis.

Data From Ministry of Well being in 2023

In line with the Eldershield Overview Committee report, 1 in 2 wholesome Singaporeans above the age of 65 could possibly be severely disabled of their lifetime. About 3 in 10 severely disabled Singapore residents may stay in extreme incapacity for 10 years or extra.

This sounds fairly miserable however it’s probably that if we cut up the Singaporeans age 65 and above into cohorts we can have extra being disabled when they’re above 75-80 years outdated than beneath. I received’t know what age that this may befall me and neither do you.

MOH up to date that greater than half of these getting payouts from CareShield Life are beneath 40 years outdated. Their age ranges from 30 to 88 with the median age being 39 years outdated. [Straits Times | Aug 2023]. MOH wish to shed mild about extreme incapacity by way of this text.

I picked out some key factors:

- Because the launch of Careshield Life, 46 individuals who had obtained payouts have died.

- In 2022, the approval fee is 73%.

- > 50% of claims not accredited didn’t full their software, together with those that died whereas assessments could possibly be accomplished.

- 25% of claims rejected was resulting from individual not assembly the incapacity standards.

Additionally they offered some information relating to the payouts:

Not like incapacity revenue, we could be relaxation assured that it may not difficult to safe a CareShield insurance coverage payout. I simply marvel why MOH couldn’t launch the age of people that begin claiming yr by yr. That can actually shed mild.

I’ve this sense that they simply need to get extra individuals who have the choice to not be on CareShield Life, that are the older cohorts, to be on it.

We all know from this sharing that:

- Fairly possible to be disabled with 3 ADLs at a comparatively younger age.

- Those that are disabled, would common 4 years.

- There are some that may last more than 10 years.

Studying from Lengthy-Time period Companies and Assist (LTSS) for Older Individuals (2022)

In my analysis, I got here throughout a latest US research that moderated my view relating to the slightly dire excessive possible Lengthy-Time period Care scenario. This paper was carried out fairly lately. The LTSS paper is to offer info to policymakers who’re fascinated by how long-term companies and helps ought to be paid for. The paper goes into how lengthy disabilities may final, what number of, and which entity will fund which proportion of the price.

The analysis creates a pc mannequin that acts like a simplified model of the true world.

- Beginning with a bunch of individuals and households that are design to be just like the precise inhabitants of the US.

- The pc mannequin then age the folks over time. Once they age, they’ll simulate issues like folks getting married, divorce, having well being issues, changing into disabled, and ultimately passing away.

- The mannequin requires actual world info to make the simulations as life like as potential.

- The mannequin doesn’t simply predict however offers a spread of potential outcomes, together with how probably it’s that somebody will want long-term take care of a short while or very long time and the way a lot it might value them.

We aren’t precisely the target market (we’re not policymakers) however I believed a few of these information is significant for us to make choices. Based mostly on the paper, I summarized the likelihood of needing care and the way lengthy within the following slide:

We break down the info to each female and male but when my function is to achieve accuracy however not precision, then breaking the info down by sexes just isn’t too completely different. The information just isn’t too completely different from the Eldershield Overview conclusion that round 40-50% don’t want long run care. I suppose they handed away by way of implies that bypass the necessity for assist (I’m not positive if this can be a good factor).

About 20-25% of these age 65 and above would wish long-term care of 5 years or longer however that vary may be rattling extensive. This appear to triangulate fairly properly with just a few different information sources. The opposite 25% is lower than 5 years.

Private Reflections about Lengthy Time period Care After Wanting on the Analysis

Out of the three questions we ponder about LTC, we in all probability get some concepts about how lengthy long run care would final however not in regards to the impact of extreme incapacity to lifespan and are there any distinction between extreme incapacity at a younger age versus older age.

I do assume that extreme incapacity in two phases is smart:

- Section 1: The low possible however excessive financial and energy influence incapacity.

- Section 2: The excessive in all probability and comparatively excessive financial influence and excessive effort influence incapacity.

If we undergo, it could be brief and manageable (lower than 5 years) or may be extra financially draining (10 years or extra).

We’d additionally know roughly the price of care in right now’s {dollars}, simply that we’re much less positive in regards to the inflation fee. The associated fee may be between $3,000 month-to-month for primary provision to $11,000 month-to-month for the upper grade nursing care. These value are earlier than any subsidies utilized.

We additionally know the common life expectancy have slowly improve previously 30 years to about 85 years outdated.

Probably the most rolled-eyes answer to my long-term care wants is to have a passive revenue from an funding portfolio right now that covers an inflation-adjusted $3,000-$11,000 month-to-month for the subsequent 60-70 years. Since it is advisable buffer for some increased than anticipated inflation fee, we will decide the capital wanted with a conservative protected withdrawal fee (learn this text to know what’s the Secure Withdrawal Price) corresponding to 2.5%.

The capital wanted will likely be about $1.4 mil to $4.8 mil right now.

That is the rolled-eyes answer as a result of not many people have this sum of cash right now and it might be totally deflating that we will solely self-assure our LTC wants (apart from insurance coverage) provided that we now have this a lot capital, apart out of your different monetary objectives.

I’d slightly body my scenario differently:

- If I do know my wealth doesn’t absolutely maintain part 1 and a couple of above, how a lot does it value right now to guard towards part 2?

- With my wealth right now, if I take into account my different monetary & life objectives, how a lot of my LTC wants may be taken care of?

I see a profit in figuring out the share of protection, slightly than I didn’t cowl 100% of the LTC wants. Share of protection is helpful for one thing like LTC as a result of even if you happen to don’t have $3,000 month-to-month, figuring out you will have revenue to cowl $1,500 month-to-month to pay for an ActiveGlobal nursing care and one thing extra is assuring in some methods.

What I dislike in regards to the story round insurance coverage safety is the binary nature of the general public dialog. E.g. You want 4-years of annual expense in essential sickness. That’s sound as a rule of thumb however some may take a look at that as an actual concern if their essential sickness protection solely covers about 1.5 years. It is best to be glad firstly that you simply might need sufficient to take one yr off if it is advisable. That’s not probably the most excellent however the first yr of a significant disaster battle could be crucial.

I felt that determining these two questions I posted is essential for me as a result of it might set my thoughts comfy that if I occur to maneuver right into a part the place I need assistance, I do know

- How a lot I want in cash (based mostly on right now’s wealth),

- that I’ve a sound and cheap plan for my caregiver,

- and to what diploma does my present wealth guarantee that, after contemplating different monetary objectives.

I’ll undergo my thought course of how I dimension up the amount of cash wanted to self-insure my long-term care wants (in right now’s wealth), the variations round it.

I may also focus on about how LTC insurance coverage comes into the image however the article could also be too lengthy and I’ll depart that to a different article.

Calculating the Capital In the present day Wanted to Self-Insure the Excessive Chance and Comparatively Costly Lengthy Time period Care Wants

I may calculate an estimate of the capital that I want right now to guarantee my LTC wants throughout outdated age, in Section 2 of what I describe earlier than with some cheap assumptions.

I feel it’s cheap that

- We’ll attempt our greatest to remain at house if we will, with the assistance of a home-based caregiver.

- If issues progressed till we now have to examine in to a nursing house, then that will likely be the price of the nursing house.

The analysis exhibits that it’s cheap that our LTC wants could also be lower than 5 years but additionally longer 10 years in some circumstances. Due to this fact, we will begin by sizing up the price by planning for a 2 part of care that final for 10 years until our median life expectancy of 85 years outdated.

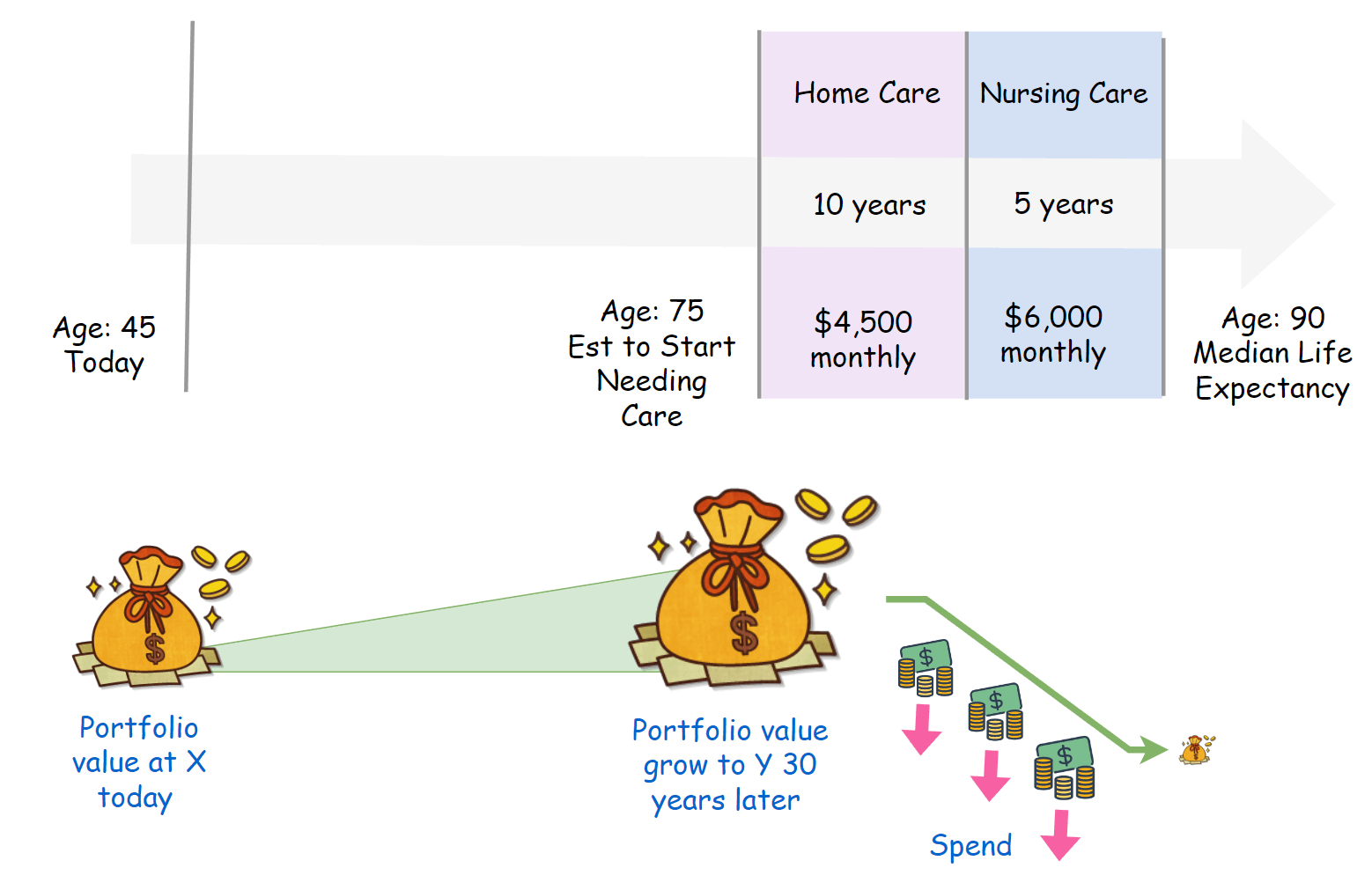

I plot the milestones, how outdated am I and the assume length within the diagram beneath:

We assume that we are going to begin needing assist at 75 years outdated which can final until 85 years outdated. The price of house care, in right now’s phrases is $3,000 to $4,500 month-to-month relying on the way you analysis. I resolve to take the figures carried out by my colleagues at Havend. These should not my very own figures. Some could query how come it comes as much as such a big determine? For those who learn my publish about my Caregiver from ActiveGlobal, it received’t come as much as half of this value however we’re additionally catering for different potential remedy value.

In distinction, the price for nursing care will look extra cheap since some readers would have skilled this. My buddy Alison (Heartland Boy) works in Orange Valley and I examine in with him how a lot a mattress value. My grandma presently resides in a nursing house and I do know the unsubsidized charges.

For those who felt that you want to a better grade of care, maybe staying in Allium Healthcare, you may modify the assumptions accordingly.

The capital we’d like right now is determined by an affordable funding and revenue system. This isn’t dissimilar from revenue planning. On this case, we’re planning for a 10-year “retirement revenue wants”, which form of implies that the protected withdrawal fee is about 7% or that we’re spending 10 equal parts until zero. We don’t want a capital to offer an revenue that final perpetually.

I’ve added the next visualization in regards to the revenue plan:

The concept is a few a part of our wealth will develop at a sure fee of return and by 75 years outdated we will withdraw an inflation-adjusted quantity to pay for the LTC wants.

There are extra assumptions then what’s illustrated so here’s what will go into the mannequin:

- Inflation of 3% p.a. from In the present day to Begin of Needing Care. The price of house and nursing are received’t keep stagnant and I challenge that to develop at 3% p.a. You could be extra pessimistic with the inflation and you would change the speed accordingly.

- Inflation/Development of 3% p.a. for revenue fee after our care wants begin. The house and nursing care value don’t remain stagnant inside that 10 years. I construct within the requirement for the revenue to develop throughout our time of want.

- An assume a portfolio progress fee of 6% p.a. from In the present day to Begin of Needing Care. I assume that I will likely be utilizing a portfolio allocation just like my Daedalus Revenue portfolio (you may seek advice from the Daedalus Revenue portfolio right here) as a result of I feel ultimately a part of Daedalus Revenue portfolio will present the revenue for this nursing care wants. It is a 85% fairness 15% mounted revenue portfolio with an ongoing value of 0.28% p.a.

- An assume a portfolio progress fee of 2.5% p.a. after our care wants begin. Why do I assume a decrease progress fee for the portfolio begin as a substitute of 6% p.a.? There are other ways of being conservative, with utilizing a Secure Withdrawal Price (SWR) being one. The opposite manner is to imagine that the speed of return to be pessimistic, nearer to a -2 commonplace deviation. Often, the returns find yourself half of the median return. Utilizing 2.5% p.a. will likely be beneath the -2 commonplace deviation. This implies the eventual capital will likely be bigger.

With these assumptions, we will calculate how a lot capital we’d like right now, in order that we will present an revenue for our long run care wants from 75 years outdated to 85 years outdated.

How A lot Capital We Want In the present day Based mostly on Totally different Inflation and Development Charges.

I made a decision that as a substitute of simply utilizing 3% p.a. inflation and 6% portfolio progress from right now until when care begins, I calculate based mostly on completely different inflation fee and portfolio progress fee to offer you some concepts:

The field that’s highlighted in yellow is the capital we’d like right now based mostly on 3% p.a. inflation and 6% p.a. portfolio progress.

If I’ve $248,311 right now and presently deploy the cash in a portfolio that may cheap give a return of 6% p.a., I ought to stand a great likelihood to have a ten yr revenue to cowl future house and nursing care.

I really feel fairly assured that I’ve this sum of cash and allotted this fashion.

I used to be fairly stunned after I got here up with the determine as a result of it seems to be rather more manageable than my preliminary fears.

We are able to body the orientation from the angle of how a lot capital you will have:

- $200,000: Coated if portfolio progress 7% p.a. and inflation fee is 3%.

- $250,000:

- Coated if portfolio progress 6% p.a. and inflation fee 3%.

- Coated if portfolio progress 7% p.a. and inflation fee 4%.

- $350,000:

- Coated if portfolio progress 5% p.a. and inflation fee 3%.

- Coated if portfolio progress 6% p.a. and inflation fee 4%.

- Coated if portfolio progress 7% p.a. and inflation fee 5%.

- $480,000:

- Coated if portfolio progress 4% p.a. and inflation fee 3%.

- Coated if portfolio progress 5% p.a. and inflation fee 4%.

- Coated if portfolio progress 6% p.a. and inflation fee 5%.

- $650,000:

- Coated if portfolio progress 4% p.a. and inflation fee 4%.

- Coated if portfolio progress 5% p.a. and inflation fee 5%.

- $900,000: lined if portfolio progress 4% p.a. and inflation fee is 5%.

The extra capital you may determine, the extra you may buffer for doubtlessly increased future inflation and doubtlessly poorer returns.

I feel I’ve the figures $350,000 and $480,000 in thoughts for the subsequent part of my evaluation. All these sums are presently decrease than my web wealth or the present worth of the Daedalus Revenue portfolio (You’ll be able to view the most recent portfolio worth on the time of writing right here).

Like I stated, these figures appeared fairly manageable contemplating that the primary fee, if we use a portfolio return of 6% and three% inflation, is $11,000 month-to-month and $17,000 month-to-month for the primary fee firstly of house care and nursing care respectively. How did this labored out?

The speed of return of 6% p.a. requires so that you can spend money on a excessive fairness portfolio and it compounded for 30 years. This isn’t one thing that an insurer can afford to allocate the cash into. You bought to belief the long run returns to occur sufficient for this plan to work.

“Kyith, masking for 10 years just isn’t protected sufficient!”

Okay, I can hear a few of you pondering about this query and I’ve positioned the analysis into how lengthy we would want the cash earlier than the plan. Nevertheless, if you happen to felt that you simply want extra margin of security in your plan, then you’ll need extra capital.

That’s all there’s to it.

As a substitute of 10 years, we will prolong the house care must 10 years and assume that our life expectancy is nearer to 90 years outdated. With such assumptions we will type a brand new desk:

For those who want to plan for a 5% p.a. inflation situation with decrease returns, you’ll need a capital of $1.36 million.

We are able to body the orientation from the angle of how a lot capital you will have:

- $250,000: Coated if portfolio progress 7% p.a. and inflation fee is 3%.

- $350,000:

- Coated if portfolio progress 6% p.a. and inflation fee 3%.

- Coated if portfolio progress 7% p.a. and inflation fee 4%.

- $500,000:

- Coated if portfolio progress 5% p.a. and inflation fee 3%.

- Coated if portfolio progress 6% p.a. and inflation fee 4%.

- Coated if portfolio progress 7% p.a. and inflation fee 5%.

- $700,000:

- Coated if portfolio progress 4% p.a. and inflation fee 3%.

- Coated if portfolio progress 5% p.a. and inflation fee 4%.

- Coated if portfolio progress 6% p.a. and inflation fee 5%.

- $1,000,000:

- Coated if portfolio progress 4% p.a. and inflation fee 4%.

- Coated if portfolio progress 5% p.a. and inflation fee 5%.

- $1,400,000: lined if portfolio progress 4% p.a. and inflation fee is 5%.

The preliminary $350,000 and $480,000 vary will nonetheless cowl a 15-year incapacity, simply not optimistically all of the situations.

For those who learn my content material sufficient, it’s possible you’ll understand that typically I’ll zoom in to very granular stuff, however I may be fairly basic and marvel how do I feel round it. On this case I’m granular in questioning about the price distinction for 10-year and 15-years and slightly broad in returns and inflation.

It’s because our lives will likely be slightly unsure. I can setup the portfolio to try to harvest a great return however there’s a lot I can not management. I’ve no management over the inflation of healthcare prices.

Reviewing based mostly on a spread of returns, inflation and based mostly on vary of capital permits me to roughly know how I’ll do given the uncertainty.

If the capital is $500,000, this covers:

- 10-12 months LTC

- Coated if portfolio progress 4% p.a. and inflation fee 3%.

- Coated if portfolio progress 5% p.a. and inflation fee 4%.

- Coated if portfolio progress 6% p.a. and inflation fee 5%.

- 15-12 months LTC

- Coated if portfolio progress 5% p.a. and inflation fee 3%.

- Coated if portfolio progress 6% p.a. and inflation fee 4%.

- Coated if portfolio progress 7% p.a. and inflation fee 5%.

It could be higher if the portfolio allocation is ready to hit a 6-7% p.a. return to cowl each a ten and 15-year LTC want and I feel Daedalus Revenue portfolio allocation covers this.

How Would I Fund the $500,000 In the present day for my Lengthy-Time period Care Wants?

It is going to come as no shock that ultimately if wanted, the cash from my long-term care will come from Daedalus Revenue portfolio, which is presently 2.8 instances greater than this quantity.

I wish to share just a few handles that will help you take into account about your individual self-insuring plans.

All of us would wish to grasp just a few ideas or framing, if not you wouldn’t belief the plan:

- Not all of your web wealth (belongings minus liabilities) right now may be thought of as appropriate to deal with your long-term care wants.

- It is best to have completely different views/allocations of your web wealth relying on the stage of life/ state of life you might be in. This implies we will re-prioritize and re-allocate cash relying on the stage of life.

- Acknowledge that there are cash that you simply can not re-prioritize as a result of they fund monetary objectives which might be extra essential to you. This will likely be much less excellent to think about as cash to cowl your long-term care wants.

- Cash that’s put aside to self-insure ought to realistically have the identical asset allocations as what the cash is used for right now.

- If a partner is severely disabled, the household will nonetheless want revenue in different areas.

That may be a checklist of concerns that may look too complicated however let me attempt to clarify aside from number one.

If in case you have a lot wealth, you would put aside this sum of cash right now, allocate the cash into an asset allocation, to maintain this. Nevertheless, I don’t assume everybody has that.

It is vital for us to acknowledge that whereas cash is fungible (which implies $1 allotted for X is similar as $1 allotted for Y), you may’t contact some huge cash for long run care wants as a result of

- The cash presently funds some obligations that ultimately your loved ones continues to be obligated to fund.

- Some cash is realistically spend down or gifted away by the point the set off even occurs.

Easiest instance is you could’t presumably liquidate a part of your residential house if you happen to want cash for long run care proper? Truly you would technically if you happen to reside in a landed property and the partner is okay to maneuver right into a two-room HDB. However I feel you get what I imply.

A few of your portfolio could also be used to generate revenue on your trip or discretionary spending. Chances are you’ll marvel by the point you want it, will the cash be there. Most likely not.

We should always take a look at this LTC wants as taking inventory how we’re doing with what we put aside for LTC wants as a substitute of setting and forgetting it. Extra on this later.

2. It is best to have completely different views/allocations of your web wealth relying on the stage of life/ state of life you might be in.

We like to take a look at how our cash help our lives as a steady line the place we add monetary objectives, hit the goal, then add extra monetary objectives, hit the goal. However it’s probably, that the set of monetary objectives modifications over time relying on the state of life that we’re in.

When our state of life modifications, we ought to fall much less to sunk-cost fallacy and take into account how we will reallocate our sources to help the subsequent part of our lives.

I’ve checklist out how we might allocate our web belongings based mostly on the stage and state of life we’re in:

I checklist out virtually 5 states and 4 of them are frequent with one that’s related to the subject we’re discussing right now. Our priorities the place we divert our financial savings change over time. We can not allocate a lot to FI as a result of we bought wedding ceremony and renovation to consider once we are youthful (first field). As we’re married with youngsters we need to save up for our FI and kids’s training so most of our sources are diverted there (second and third field).

Some could also be confused how to consider their legacy wants. I feel that’s principally fascinated by their wealth right now… and what you want to do when each your partner and your self just isn’t round (the final field).

Via these life modifications, you are attempting your greatest to make the perfect monetary choices with the sources that you’ve.

What we failed to essentially plan is the state the place considered one of us is disabled whereas the opposite individual is alive and properly. This may be whereas we’re accumulating or decumulating. The forth field greatest illustrates this. When one partner is disabled, probably the most smart factor is you need to see methods to reallocate your loved ones sources to assist:

- A few of the FI revenue ought to be diverted over.

- Household ought to get some revenue from Careshield Life.

- Grownup youngsters ought to assist out.

- Select to lease out a room or downgrade.

These are all capital reallocation choices.

Would reallocation give us a profitable end result? I wish to assume we’re all versatile and resilient however you may as well take into account and check out your greatest to plan for this part of life as a lot as you may in order that the household can do okay.

3. Acknowledge that there are cash that you simply can not re-prioritize as a result of they fund monetary objectives which might be extra essential to you.

If you’ll be able to re-frame and have completely different planning snapshot based mostly on the state and stage of life you might be at, you be shifting to think about what are the belongings that you could be re-prioritize if considered one of you finally be disabled and what wouldn’t.

Firstly, there are some belongings that you wouldn’t promote and are simply meant for some evergreen objectives. Your residential house could also be one. As a single, my member of the family can at all times take into account renting out two of my rooms, or to dump the house if the appointed donee has energy of legal professional to make choices on the residential property. So the house is extra subjective right here.

A greater instance will likely be CPF Medisave funds. Medisave is supposed on your medical wants and even if you happen to want to divert, you can’t do it.

One other instance is how a lot of your revenue in monetary independence that you simply spend on discretionary stuff like trip that’s round right now, will likely be round 30 years from now?

This may be difficult for a lot of of you since you take into account your revenue in a single bunch… say $10,000 month-to-month. This contains your rigid important spending, extra versatile primary spending and your discretionary spending and even your buffers to easy out the revenue.

Is it protected to say I’ve $10,000 month-to-month revenue right now, due to this fact my LTC wants is taken care of?

Not at all times the case.

- Some plan for revenue that steps down over time.

- Some spend a higher proportion on important spending whereas others have a higher proportion on discretionary.

You would wish to see if you happen to can separate out every $1 right now to determine realistically you may reallocate the sources if one partner is disabled.

I’ve much less downside right here as a result of I at all times take into account my important, primary spending and discretionary spending to return from completely different portfolios so I’ve a clearer view how a lot is the portfolio just a few years from now evaluate to somebody who take a look at issues simplistically.

4. Cash that’s put aside to self-insure ought to realistically have the identical asset allocations as what the cash is used for right now.

I felt this one is kind of self explanatory.

In case your plan is for $200,000 to develop to $X in 30 years time, the cash right now, allotted maybe to different stuff, should be deployed to equal belongings that has the potential to earn that very same quantity. For those who presently have it in money, it might’t presumably develop on the similar fee. So how can the plan be life like?

5. If a partner is severely disabled, the household will nonetheless want revenue in different areas.

Whereas I’m single, this can be a consideration for the parents who’re married however it form of applies to me in a sure manner.

We can not assume that if an individual is disabled their different spending goes away:

- A few of your discretionary spending ought to be diminished,

- however your partner could should spend usually on his or her necessities,

- the household must pay the often utilities, conservancy or MSCT, and upkeep & repairs value.

The problem for us is that every one of those happen years from now however presently, the cash could exist as your monetary independence fund in a single lump sum. So how do you cut up them out?

In some unspecified time in the future, you may not be capable of. If you’re presently 32 years outdated and the cash that you simply put aside on your monetary independence is $105,000, you may not have sufficient on your eventual monetary independence at this level. Technically, you would say 30% of your revenue wants right now is one thing that you simply can not scale back even in case you are severely disabled sooner or later, however it’s powerful to ascertain it proper now.

This train will make extra sense if the cash that you’ve, apart out of your extra essential objectives that can not be reclassified for long-term care is $700,000-$800,000. Technically, if we use a 3% protected withdrawal fee (SWR) as a rule of thumb, the present revenue is estimated at $1,750-$2,000 month-to-month, you may ponder how a lot realistically, are revenue for upkeep repairs, and the way a lot capital is left for potential long run care wants.

For those who take a look at how the capital wants triangulate round $250,000, $350,000, realistically your portfolio for FI ought to alleviate your LTC wants, along with Careshield Life, CPF LIFE.

Must you evaluation your present bills intimately? I feel if you happen to do, you may cut up them higher. Usually, I feel apart from what’s take into account important, discretionary spending, and buffers to easy out the revenue, you may body your spending for LTC planning this fashion:

When each of you might be alive, whether or not in decumulation or accumulation mode, there will likely be some a part of spending that’s household spending that’s slightly important and recurring. This can be utilities, broadband, recuring fund for upkeep, conservancy and MCST, property tax. There may be another stuff that you simply discover it to be recurring corresponding to serving to out a member of the family. These are issues that can’t reduce down.

Past that, a lot of the fundamental, important and discretionary spending is eat as a pair.

When one partner has to care of his or her disable wants, his or her portion may be diverted for his wants leaving sufficient revenue for the household and partner spending. Would there be a scenario the place each partner consecutively want long run care wants? I discover that difficult to imagine and in that case there’ll nonetheless be some household spending that should pay for.

Is there a share rule of thumb to estimate the ratio between the household spending and our personal spending?

We set a tough rule of 70% personal spending and 30% household spending. It’s a tough rule and your individual private mileage can be completely different. For instance, Kyith can not apply this rule in any respect contemplating how I construction my spending.

Why I Assume it’s Wise {that a} Portion of Daedalus Revenue Portfolio In the present day May be the Capital for Future Lengthy Time period Care Wants

Daedalus is roughly valued at $1.45 million at this level and it’s suppose to offer revenue if I retire for my important spending ($854 month-to-month) and primary spending ($430 month-to-month) primarily. If we take the mix annual quantity divide by the present portfolio worth, the present withdrawal fee is 1%.

Having a protected withdrawal fee of decrease than 2% is already very conservative and in fact this implies I may presumably divert 50% of Daedalus for my different objectives (corresponding to LTC wants) however I feel I don’t need to make large actions apart from spending from the portfolio sooner or later. That is in order that readers can have a great reference level.

If in case you have a protected withdrawal fee decrease than 2.4% while you begin drawing the revenue, chances are high 30 years later, the true worth (means inflation-adjusted worth) of your portfolio ought to nonetheless be the identical.

This implies if I simply spend however inside an affordable spending choice tree by the point 30 years later, the capital ought to be intact. I do count on Daedalus portfolio to offer revenue perpetually.

The portfolio is presently allotted in an asset allocation just like my assumption that ought to present 6-7% p.a. return.

For those who take out $500,000, the residual portfolio can nonetheless present my most important spending, which incorporates all the upkeep spending corresponding to property tax, utilities, conservancy charges, upkeep.

What then about Section 1: The Low Possible however Excessive Financial Incapacity?

What I discussed up to now handle extra of Section 2.

Section 1 is harder as a result of:

- You don’t know if a incapacity is short-term or everlasting.

- Whether it is everlasting for a youngster, the price can be fairly troublesome to take care of. Chances are you’ll want to arrange to take care of a 30-year want.

A few of my insurance coverage will cowl this:

- Complete Everlasting Incapacity [Probably $450,000 payout | Ends at 65]

- Incapacity Revenue [Cannot work: $2,000 monthly till 65 | Ends at 65 or no work]

- Important sickness [Probability $350,000 payout (will overlap with some of the TPD]

- Careshield Life revenue [Currently at S$664 monthly]

If I apply a preliminary withdrawal fee of three% on Daedalus, this may herald an revenue of $3,625 month-to-month.

I feel I ought to be lined to a sure extent.

My present plan is when i’m working I’d procure a Singlife Careshield complement to be extra properly lined.

I would depart the insurance coverage to half 2 of my private long-term care protection notes.

Meantime, let me spend a while addressing some potential questions that you might have.

Why Did you Use S$4,500 month-to-month and S$6,000 month-to-month when Future Care Value Could be Increased?

For those who take a look at the assumptions constructed into the desk of preliminary capital required, it embeds an inflation fee of three% p.a. earlier than the spending is doubtlessly wanted and likewise 3% p.a. progress of the revenue when the spending begins. Because of this I’ve factored inflation into the plan.

I offered completely different capital if you happen to want to imagine a better inflation value as properly.

Wouldn’t Assuming a Price of Return of 6% be Too Optimistic?

The speed of return just isn’t extraordinarily optimistic for a predominately fairness portfolio. If I’m unfortunate for 30 years, the speed of return could be decrease at 4% p.a. after 30 years however I additionally can not do something in regards to the plan that may enhance the chances. Possibly you would.

Would the revenue then be decrease? Sure that may be.

This is the reason I’ve a watch on $500,000 in preliminary capital to cowl the LTC wants as a substitute of $350,000 or $280,000 simply to be a little bit conservative. For those who take a look at the quantity assume for house care, you may additionally understand it’s a tad excessive. I feel there are some margin of security in that.

Returns sooner or later are unsure however we will plan round that uncertainty systematically.

Why Do You Plan with Preliminary Capital In the present day As a substitute of Passive Revenue?

Effectively you would if you happen to want to specific it that manner.

I current worth the revenue stream wanted for house care and nursing care from 75 to 85 years outdated as a result of I plan for a slightly brief interval of 10 years. Whether or not I exploit a protected withdrawal fee to estimate the revenue, it really works out to be roughly 5 x the preliminary revenue stream for house care + 5 x the preliminary revenue stream for nursing care. Principally no distinction.

For those who want to, you would estimate how a lot of your residual revenue out of your portfolio, CPF LIFE, and different means may be use to pay on your house care or nursing care wants when the time comes.

However I think while you plan for these revenue on your monetary independence, you will have construct in some margin of security in your revenue to easy out the revenue volatility. You additionally need the cash to final for a very long time (most definitely outlast you and you’ll cross down the cash).

However your long run care wants could be a finite variety of years.

I’m on the lookout for a solution exploring the ground of the capital that I want minimally in order to determine if I’m adequately self-insured. I’m on the lookout for a extra optimized reply.

In case your revenue stream is so extensive, you should utilize that 70%:30% ratio, after which divide by 2 to see if your loved ones is sufficiently lined for long run care individually.

You may additionally have to leap just a few psychological hoops in case your revenue stream is fairly staggered.

Don’t You Discover the $4,500 Month-to-month Revenue Want for House Care A Tad Bit Too Excessive?

I took the $4,500 month-to-month from home-based care information offered internally. For those who ask about my private expertise (I employed a caregiver for my late-dad earlier than, and have a tendency to my late-mom. I paid partially for the nursing house take care of my grandmother), I can not join with that determine.

For those who inform me a sum of $2,200 month-to-month that does plenty of issues. I suppose the $4,500 month-to-month bake in plenty of remedy and rehab.

The alternate query is: Kyith, does it make sense for me to plan for 50% much less?

The problem is I don’t know by having much less revenue and fewer remedy would that stop you from bettering your incapacity.

However if you happen to want to use $2,200 month-to-month in order to determine what’s a decrease flooring that you simply may be capable of reside with, you would do this. Suppose we use the identical 3% inflation, and 6% p.a. portfolio return, and hold the nursing care to $6,000 month-to-month, as a substitute of $248,311 in preliminary capital, the quantity turns into $189,419 in preliminary capital, $59k or 24% lesser.

I feel that’s vital to some however much less vital to me.

Would You Take into account Renting Out a Room or Your House to Offset Nursing Care Prices?

I may doubtlessly do this.

That will not be out of query. A house round my space rents for $3,000 month-to-month. This could doubtlessly offset the price of nursing care. This works for me as a single presently, however that may not give you the results you want.

Nevertheless, my caregiver must rigorously take into account which is extra price it. If there is no such thing as a revenue coming in, and if correctly means-tested, my nursing care value may doubtlessly fall from $5,000 month-to-month (in todays’ {dollars}) to $500-$1,000 month-to-month.

Which brings us to the subsequent level.

Wouldn’t There Be Some Subsidies That Might Cut back The Value of Care Within the Future?

There are.

If my month-to-month per capita family revenue (PCHI) is zero (as a single), I’m a Singapore Citizen and the annual worth of my house is lower than $21,000, the subsidy for Residential LTC companies is 75%. [Subsidies for Residential Long-Term Care Services]

I’ve seen this quantity be diminished to $500 month-to-month or $1,000 month-to-month

Apart from that there’s additionally House Caregiving Grant that acknowledges caregivers’ contributions and reduces caregiving prices, with month-to-month payouts of as much as $400 per 30 days. That is extra for home-care. We are able to take into account $250 month-to-month as a substitute of $400 month-to-month if we had been to consider inflation, which can scale back that $2,200 decrease flooring month-to-month to $1,950 month-to-month.

If we take into account nursing care of $1,000 month-to-month and residential care of $1,950 month-to-month, this will scale back the preliminary capital from $248,311 to $72,111.

Now that could be a rather more inexpensive sum.

Nevertheless, I don’t assume I’m the kind who would plan based mostly as if the federal government subsidy construction will likely be related in 30 years time. That is form of just like the concept inflation previously is 2% p.a. for 20 years so subsequent 50 years, Singapore inflation would common that.

I feel I’d slightly evaluation if we don’t rely a lot on subsidy, how a lot would that value me.

Conclusion

What? Nothing on our favourite Careshield Life, Eldershield and its dietary supplements?

I feel half 1 will discover if we now have some web wealth presently, how a lot would it not value us to self-insure towards the excessive possible and excessive financial influence part of extreme incapacity. We’ll discover the insurance coverage half partly 2 (if I ever get better from penning this).

Personally, I’m glad I get to take part on this solutioning because it forces me to discover methods to make sense of my future long run care wants. If we didn’t maintain our long-term care wants, we will at all times rely upon our caregivers to assist finance that.

This isn’t new. Prior to now and presently, I’ve financed to completely different diploma relations long run care. However wouldn’t or not it’s higher if we will do our half?

I feel that is the primary article out in public about long run care that isn’t about insurance coverage, Careshield or Eldershield however on self-insuring. Insurance coverage could be the extra environment friendly methodology however increasingly, I feel the extra elementary sound framework to wealth is one the place you insure earlier than you construct up your wealth however construct medical sinking fund in order you be in management about how you should utilize the cash on your healthcare wants.

Leverage on insurance coverage while you haven’t construct up the wealth and the results are bigger as a result of many individuals rely upon you or time is extra essential.

My essential fear is whether or not I’ve sufficient for the excessive in all probability and excessive financial influence extreme incapacity in later years. Based mostly on my mannequin, I ought to be fairly properly lined with some margin of security.

I felt relieved the numbers look extra manageable and I’ve a strategy to self-fund with my present sources. And I hope that by sharing a few of my thought course of, it might assist you to dimension up how a lot you want for your loved ones as properly.

For those who discover this sharing helpful, take into account sharing it with anyone.

You’ll be able to learn my different notes about my very own private planning beneath Managing Kyith – My Private Notes.

If you wish to commerce these shares I discussed, you may open an account with Interactive Brokers. Interactive Brokers is the main low-cost and environment friendly dealer I exploit and belief to take a position & commerce my holdings in Singapore, the US, London Inventory Alternate and Hong Kong Inventory Alternate. They permit you to commerce shares, ETFs, choices, futures, foreign exchange, bonds and funds worldwide from a single built-in account.

You’ll be able to learn extra about my ideas about Interactive Brokers in this Interactive Brokers Deep Dive Sequence, beginning with methods to create & fund your Interactive Brokers account simply.

Kyith is the Proprietor and Sole Author behind Funding Moats. Readers tune in to Funding Moats to be taught and construct stronger, firmer wealth foundations, methods to have a Passive funding technique, know extra about investing in REITs and the nuts and bolts of Lively Investing.

Readers additionally comply with Kyith to discover ways to plan properly for Monetary Safety and Monetary Independence.

Kyith labored as an IT operations engineer from 2004 to 2019. At the moment, he works as a Senior Options Specialist in Insurance coverage Begin-up Havend. All opinions on Funding Moats are his personal and doesn’t symbolize the views of Providend.

You’ll be able to view Kyith’s present portfolio right here, which makes use of his Free Google Inventory Portfolio Tracker.

His funding dealer of alternative is Interactive Brokers, which permits him to spend money on securities from completely different exchanges all around the world, at very low fee charges, with out custodian charges, close to spot foreign money charges.

You’ll be able to learn extra about Kyith right here.